As recently as 2022, China/Hong Kong accounted for over 35 percent of global beef imports.

Derrell S. Peel, Oklahoma State University

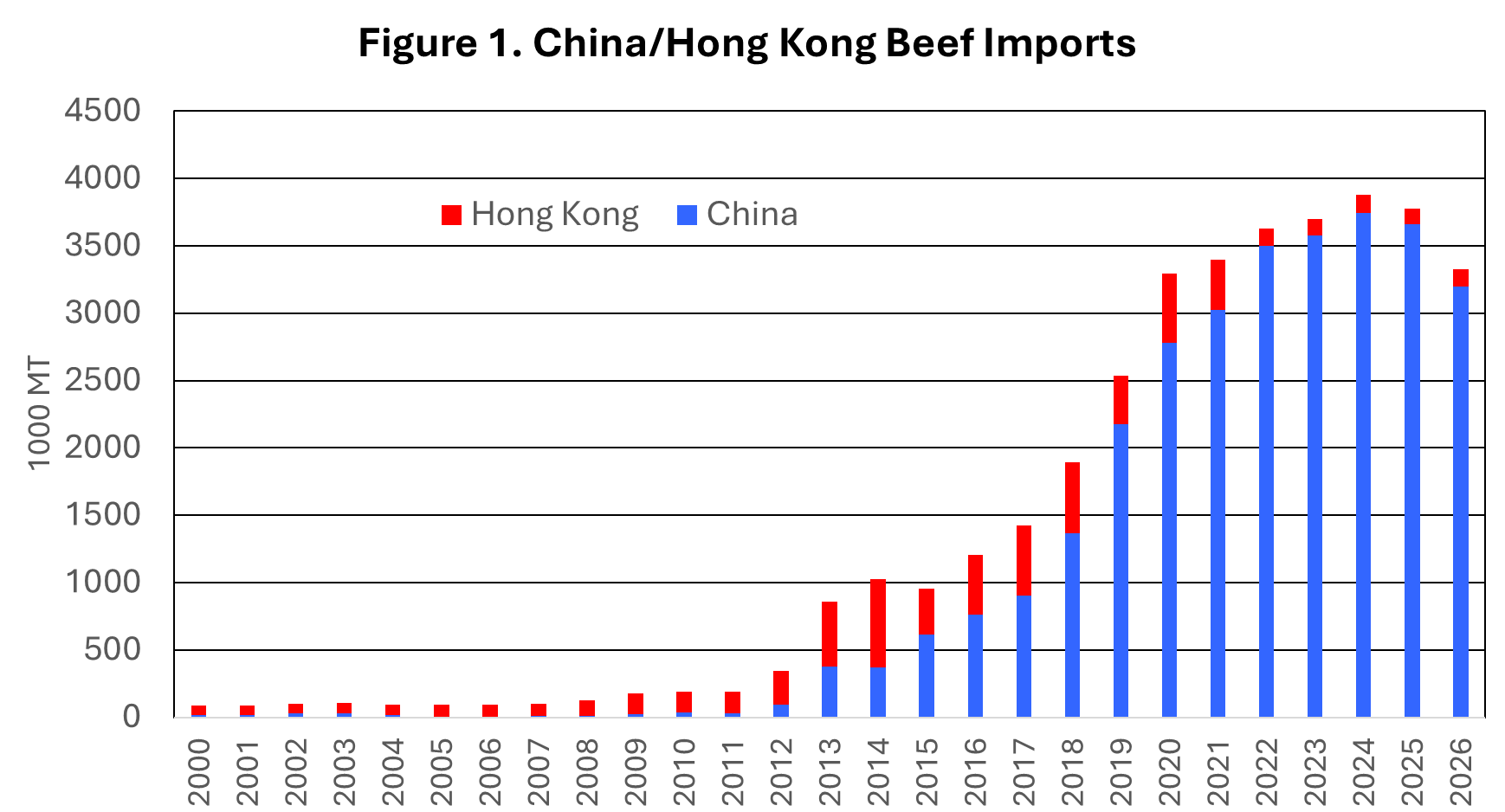

The role of China in global beef markets has changed rapidly in the past two decades. China (including Hong Kong) was not a player at all in global beef markets as little as fifteen years ago but has risen rapidly to become the largest beef importer in the last decade (Figure 1 above). For many years, China was a large beef producing and consuming country but had almost no presence in global beef markets. Starting about 2013, rising beef consumption in China began to exceed domestic beef production leading for the first time to significant beef imports.

Although per capita beef consumption in China remains relatively low, roughly 13 pounds compared to 59 pounds in the U.S., the large population means that small increases in beef consumption represent large amounts of beef in total. As a result, China/HK quickly became the largest beef importing country, surpassing the U.S. by 2017 (Figure 2). As recently as 2022, China/HK accounted for over 35 percent of global beef imports.

Part of the growth in beef imports in China/HK included increased exports of U.S. beef to China. Hong Kong was a significant beef export market in the 2010s, representing as much as 16 percent of total U.S. beef exports, and was the number three export market. It was generally recognized that a portion of exports to Hong Kong were subsequently transshipped into China. After the U.S. achieved official access to China, beef exports began to grow, with exports to Hong Kong decreasing as expected (Figure 3). For this reason, data from China and Hong Kong are combined, although still reported separately.

In 2025, with tariffs in place and U.S. access to China revoked, exports to China/HK decreased sharply, although beef exports to Hong Kong increased to slightly offset the total decrease (due to different political responses in Hong Kong). The China/HK share of U.S. beef exports dropped from 18.7 percent (third largest) to 10.4 percent of total beef exports and fourth place among beef export destinations (Figure 4).

While China/HK quickly grew to be a major U.S. beef export market after 2020, the U.S. share of total China/HK beef imports has been relatively small. The U.S. share of total beef imports in China/HK peaked at 8.8 percent in 2022 and dropped to 3.7 percent in 2025. There is no doubt that China/HK generally represents significant beef export potential for the U.S. in the absence of political barriers.

Figure 4 shows the dramatic loss of China/HK beef exports in 2025 relative to other major beef export markets. Decreased beef exports to China/HK accounted for 68 percent of the total decrease in U.S. beef exports in 2025. The impact of this loss in U.S. beef market was largely unrecognized simply because the domestic U.S. market was so strong and trending higher. Under different market circumstances, the impact would be much more evident. Part of the future prospects for herd rebuilding and increased beef production in the U.S. will depending on maintaining and building robust beef export markets and China/HK will certainly be a key component.