With cattle inventories unlikely to grow much, if any, in the next couple of years, it is not clear whether additional packing sector adjustments will be needed.

Derrell S. Peel, Oklahoma State University

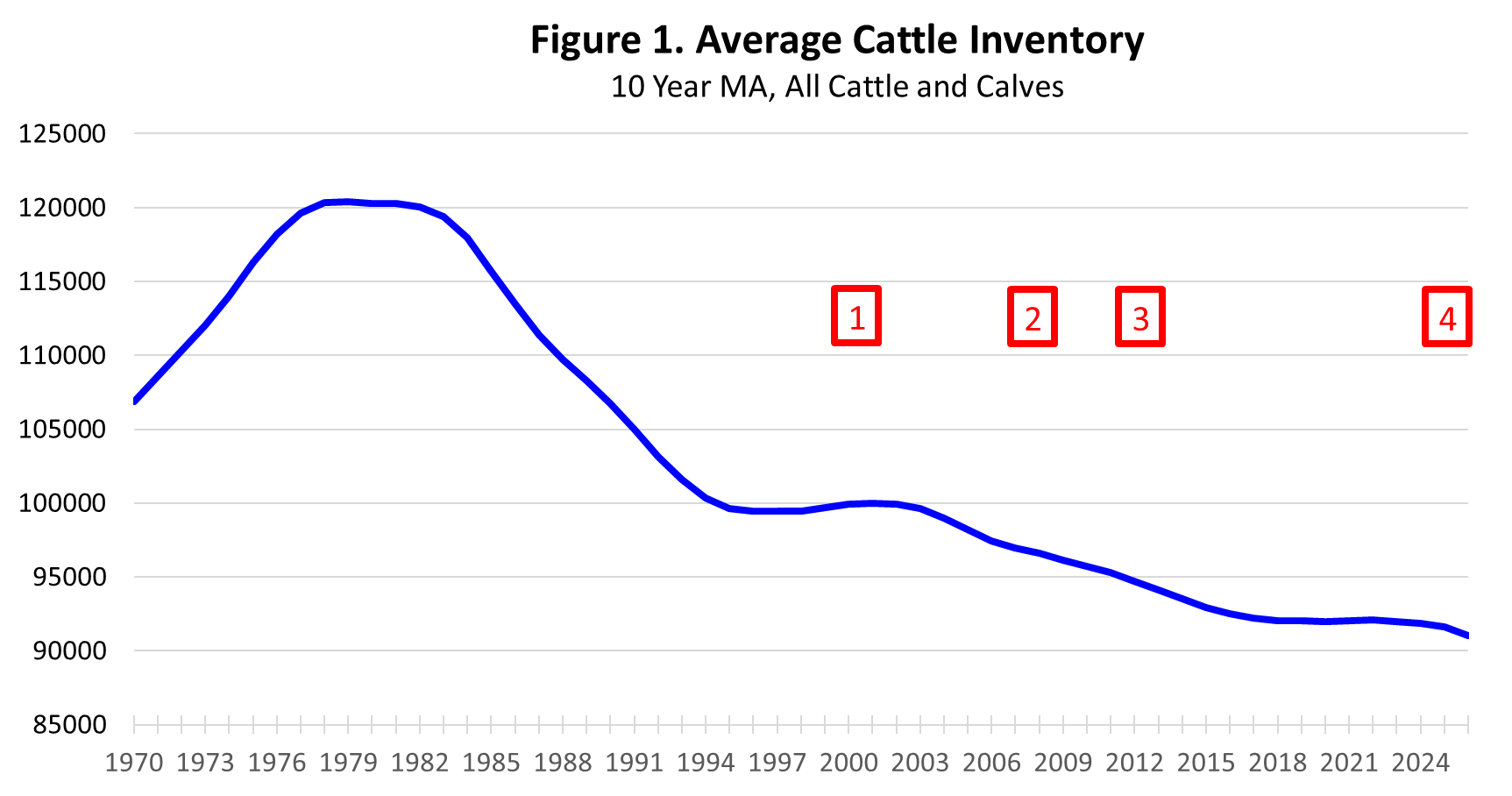

Recent announcements of facility closures from the beef packing highlight the continuing challenges that low cattle inventories pose for the beef industry. Beef packing represents large investments in facilities and a long-term perspective. Adjustments in packing capacity occur slowly and are not just the result of current cattle inventories but the cumulative impacts over time. Figure 1 above shows how average cattle inventories have decreased over time.

The majority of beef packing capacity was built from the 1960s into the 1980s when average cattle inventories were 20-30 million head larger than today. Adjustments to packing infrastructure occur slowly and abruptly with different regional impacts. The numbered boxes in Figure 1 correspond to the major adjustments to fed packing capacity in the past 26 years:

1: ConAgra plant burned, 2000, Garden City, KS (plant not rebuilt)

2: Tyson plant closed, 2008, Emporia, KS

3: Cargill plant closed, 2013, Plainview, TX

4: Tyson plant in Lexington NE closed/Amarillo TX plant reduced, 2026

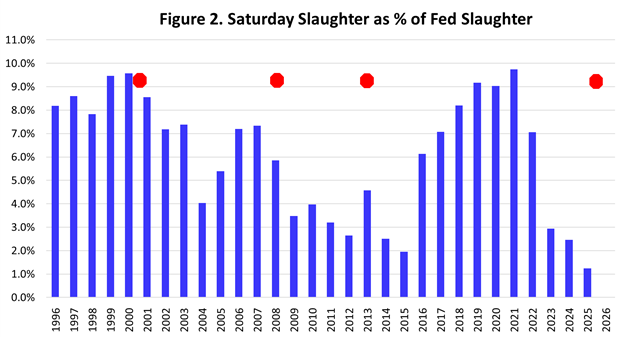

With both plant numbers and capacities fixed in the short run, Saturday slaughter is the principal source of flexibility for the packing industry to adjust to short run changes in cattle numbers. Figure 2 below shows Saturday slaughter as a percentage of total slaughter for the past thirty years (red symbols correspond to plant closures). When cattle numbers are insufficient, the Saturday Slaughter percentage decreases. The previous cyclical low in cattle inventories prompted generally low Saturday slaughter rates from 2009-2015. The one-year bump in 2013 was likely the result of the plant closure that year.

Low Saturday slaughter rates since 2023 show the impact of current low cattle inventories on the packing sector. The 2025 Saturday slaughter rate of 1.2 percent is the lowest in the past thirty years. The recent plant closure and reduction by Tyson will provide some relief in 2026. With cattle inventories unlikely to grow much, if any, in the next couple of years, it is not clear whether additional packing sector adjustments will be needed.

Derrell Peel discusses the current cattle market outlook and explains why boxed beef prices may trend higher as spring approaches on SunUpTV from March 14, 2026